DSS Inc. (NYSE: DSS) Due Diligence and H2 2023 Forecast

Everyone loves dividends and other kickbacks for shareholders that sweeten the deal on an investment position. One company I’ve recently added to my portfolio is DSS Inc. (NYSE: DSS), a dynamic small cap player that is expecting major catalysts over the remainder of 2023 and which offers a promising multibagger opportunity. The company’s business model is a bit complex, so today I’m posting an in-depth due diligence analysis on DSS that explains why I think it’s trading at a significant discount with a forecast for robust growth on the short-term horizon.

First off, a bit about how this company ticks. DSS generates shareholder value by acquiring, developing, and spinning off subsidiaries that translate into dividends and share distribution for investors. To date, the company is composed of nine distinct business segments, three of which the company has announced plans to spin off over the course of the next year. The table below summarizes these different subsidiaries:

With its strategic investments and diverse business structure, DSS Inc. aims to drive growth and success across these sectors while hedging risk and gaining exposure to a number of different sectors. According to their most recent investor deck, the net asset value of DSS’ portfolio was $182M as of end-Q3 ‘22.

In terms of its bottom line, the Q1 2023 financials the company released in May paint an encouraging picture of profitability and cash flow. According to the report, DSS achieved significant growth in revenue in some of its key segments, particularly in its Premier Packaging subsidiary, where sales of printed products increased by 72% compared to the same period in 2022. The company also saw an improvement in operating loss, which decreased by 24% in Q1 2023. Additionally, there was a decrease in both the cost of revenue (4%) and total cost and expenses (16%) in March 2023 compared to March 2022. DSS Inc. experienced a notable increase in net cash from investing activities, rising by 115% in March 2023, primarily due to the sales of marketable securities totaling $11,330,000. These financial highlights reflect the company’s strong performance and effective cost management strategies during the first quarter of 2023. Furthermore, with $13.7M cash in the bank at the end of Q1, DSS has the capital needed to pursue its aggressive spin-off strategy slated for the remainder of the year.

And now to a discussion of DSS’ spin-off strategy. Earlier this year, the company spun off Sharing Services Global Corporation (OTC: SHRG), which drove a double-digit jump in DSS share price over the following week as well as the distribution of 280M shares valued at $5M of ±$0.02/share. At the time of the share distribution, SHRG was pursuing a NASDAQ uplisting, signifying that this initial tranche of shares can be expected to accumulate significant value over time. One important take-away from the Q1 spin-off of SHRG is that it benefited DSS shareholders by increasing share price as well as providing the added perk of fresh shares.

Looking forward, a second spin-off is slated for as early as next week–that is, June 30th, 2023. Impact BioMedical is a development-stage biotech company working on a number of OTC solutions for everything from antivirals to mosquito protections to alternative sugar products (see table below for the full portfolio). Zacks’ SCR recent coverage forecasts the Impact Biomedical IPO to generate up to $50M, which they argue has the potential to catapult DSS share price to as much as $1.00 for a value multiplying effect of >4X from its current value. As was the case with SHRG, DSS plans to similarly distribute shares to augment the added value investors will receive from this spin-off.

Looking towards Q3/4 ’23, DSS has two additional spin-offs in the works:

- American Bancorp: Zacks SCR assesses this as the most spinoff-ready subsidiary after Impact Biomedical, with a possible IPO date of Q4 ’23. Given the fact that it holds $40M in outstanding loans, a standard valuation for listing would be in the range of ±$150M. This too is likely to exert a meaningful bullish impact on DSS share price.

- American Medical REIT, a real estate investment trust targeting healthcare facilities in secondary and tertiary markets. Though the REIT spin-off may be pushed to early 2024 due to rising interest rates, the company is aiming for the subsidiary to reach a sizable valuation of $200–250M before pursuing a listing.

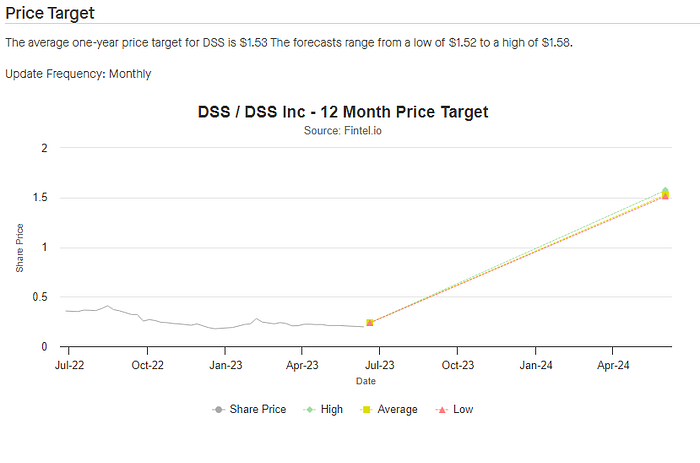

Taking these three planned spin-offs into account, analysts are highly bullish on the future trajectory of DSS share price. Zacks SCR’s price target is $1.50, which translates into around 500% upside for current shareholders.